Loan repayments can feel manageable at the beginning, but over time, high interest rates or rigid repayment terms may start putting pressure on monthly finances. Many borrowers continue paying expensive loans simply because switching feels complicated or risky. In reality, this is where a balance transfer loan can make a real difference.

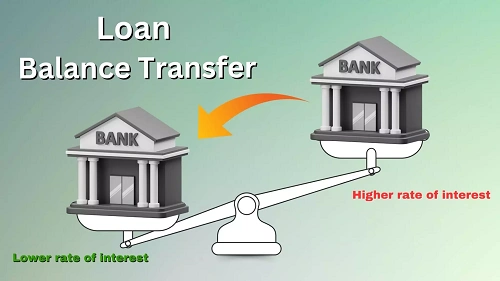

A balance transfer loan allows you to move your existing loan from one lender to another—usually to get a lower interest rate, better repayment terms, or improved service. It is a refinancing option designed to reduce overall loan cost and make EMIs more comfortable. When used correctly, it can save a significant amount of money. When used without proper evaluation, it can lead to unnecessary charges and complications.

This article explains what a balance transfer loan is, its key features, benefits, and limitations in a clear and practical way.

What Is a Balance Transfer Loan?

A balance transfer loan is a facility that allows a borrower to transfer the outstanding balance of an existing loan from the current lender to a new lender. The new lender pays off the old loan, and the borrower continues repayment with the new lender under revised terms.

Balance transfers are most commonly used for home loans, personal loans, car loans, and loan against property. Borrowers usually opt for this when the new lender offers a lower interest rate, longer tenure, or more flexible repayment options.

Key Features of Balance Transfer Loan

1. Transfer of Outstanding Loan Amount

Only the remaining loan balance is transferred, not the original loan amount. The borrower starts repayment with the new lender based on the transferred balance.

2. Lower Interest Rate Opportunity

The main feature of a balance transfer is the possibility of securing a lower interest rate, which reduces EMIs or total interest cost.

3. Flexible Repayment Tenure

Borrowers may choose to reduce EMI by extending tenure or reduce total interest by keeping tenure shorter.

4. Applicable to Multiple Loan Types

Balance transfer facilities are available for home loans, personal loans, car loans, and secured business loans.

5. Option for Top-Up Loan

Some lenders offer an additional top-up loan along with the balance transfer, based on eligibility.

6. Structured EMI Repayment

Repayment continues through fixed EMIs, similar to the original loan, but under revised terms.

Benefits of Taking a Balance Transfer Loan

1. Reduces Interest Burden

Lower interest rates can significantly reduce the total interest paid over the remaining loan tenure, especially for long-term loans.

2. Lower Monthly EMI

Borrowers can reduce EMI amounts, easing monthly cash flow and improving financial comfort.

3. Improves Loan Terms

A balance transfer may offer better customer service, clearer terms, or more flexible repayment options.

4. Option to Restructure Loan

Borrowers can realign tenure and EMI structure according to current income and future plans.

5. Opportunity for Additional Funding

Eligible borrowers may receive a top-up loan along with the transfer, meeting extra financial needs at a lower rate.

6. Better Financial Control

Switching to a better loan structure can help improve budgeting, savings, and long-term financial planning.

Limitations of Balance Transfer Loan

1. Processing and Transfer Costs

Balance transfer involves charges such as processing fees, legal fees, valuation charges, and stamp duty, which reduce net savings.

2. Eligibility and Credit Assessment

Approval depends on credit score, income stability, and repayment history. Not all borrowers qualify.

3. Time and Documentation

The process requires paperwork, verification, and coordination between lenders, which can take time.

4. Limited Savings in Late Loan Stage

If most EMIs are already paid and loan is near completion, interest savings may be minimal.

5. Risk of Longer Tenure

Extending tenure to reduce EMI increases total interest cost over the long term.

6. Temporary Promotional Rates

Some lenders offer low introductory rates that may increase later, reducing expected benefit.

Who Should Consider a Balance Transfer Loan?

A balance transfer loan is suitable if:

- Interest rate difference is significant

- Loan is still in early or mid-stage

- Processing costs are outweighed by savings

- Credit score and income are strong

- You want to reduce EMI or total interest

It may not be worthwhile for small loan balances or loans close to completion.

Important Points to Check Before Opting for Balance Transfer

- Net savings after all charges

- Revised EMI and tenure impact

- Interest rate structure (fixed or floating)

- Prepayment or foreclosure charges

- Long-term repayment plan

Balance transfer should be a calculated decision, not an emotional one.

Conclusion

A balance transfer loan can be a smart financial move when interest rates fall or when better loan terms become available. It offers the chance to reduce EMIs, save on interest, and restructure repayment to suit current financial conditions.

However, it is not always beneficial. Processing costs, eligibility requirements, and tenure changes must be carefully evaluated. Switching loans without calculating total savings can result in little or no benefit.

Before opting for a balance transfer, borrowers should do a clear cost-benefit analysis and ensure the savings justify the effort. When done at the right time and for the right reasons, a balance transfer loan can significantly improve financial comfort and long-term savings.